Understanding Loan Modification

A loan modification is a permanent change to one or more terms of a borrower’s mortgage. The goal is to make the monthly payments more affordable and sustainable over the long term. Unlike refinancing, which replaces an existing loan with a new one, a loan modification alters the original loan agreement. This process is typically negotiated between the borrower and the lender, often with the assistance of a housing counselor or legal advisor.

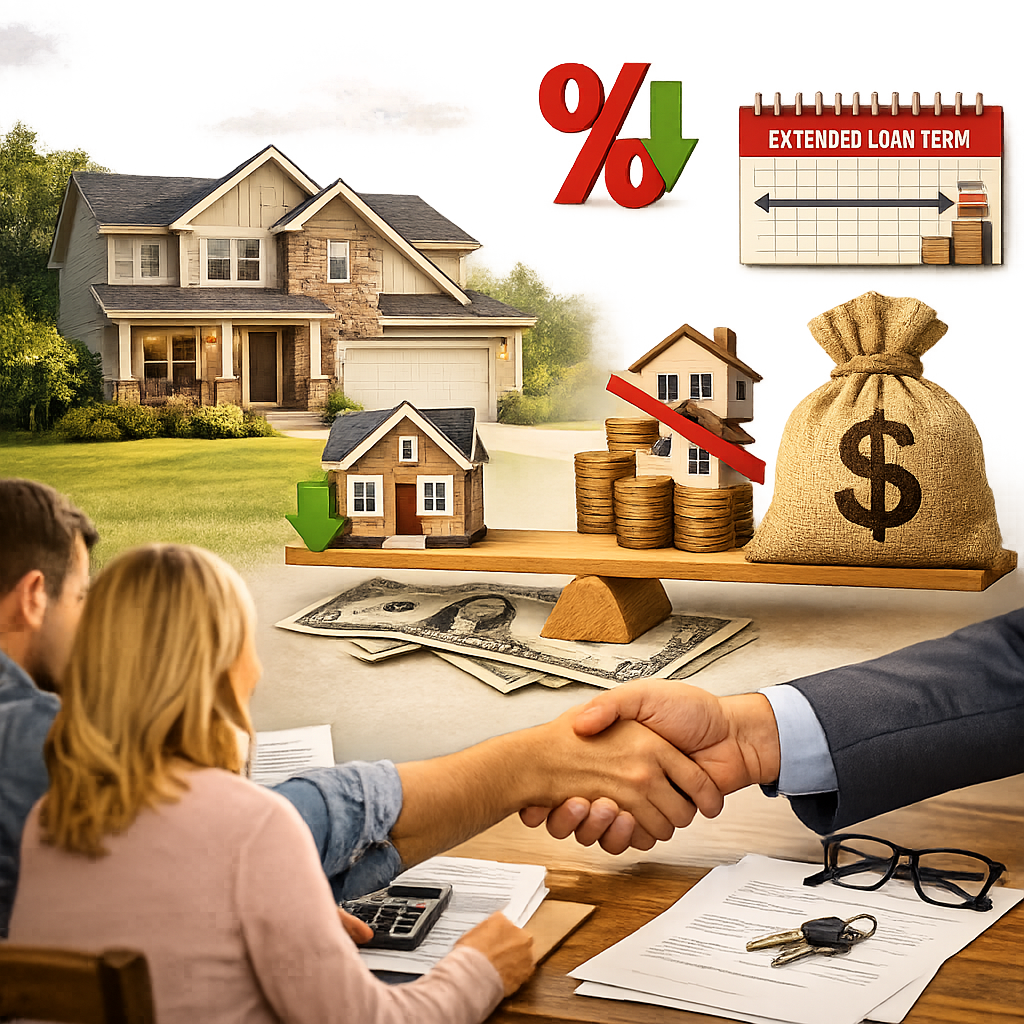

How Loan Modification Works

The modification process begins when a borrower contacts their lender to explain their financial hardship. Lenders usually require documentation such as income statements, tax returns, and a hardship letter detailing the reasons for financial distress. Once the lender reviews the application, they may offer one or more of the following adjustments:

- Interest Rate Reduction: Lowering the interest rate to reduce monthly payments.

- Loan Term Extension: Extending the repayment period to spread out payments over a longer time.

- Principal Forbearance: Temporarily deferring a portion of the principal balance to be paid later.

- Principal Reduction: In some cases, lenders may forgive a portion of the principal to make the loan more manageable.

Benefits of Loan Modification

Loan modification offers several advantages for both borrowers and lenders. For homeowners, it provides an opportunity to avoid foreclosure, protect their credit score, and remain in their homes. For lenders, it helps minimize losses associated with foreclosure proceedings and property resale. Additionally, loan modification can stabilize neighborhoods by reducing the number of vacant or foreclosed properties.

Eligibility and Considerations

Not all borrowers qualify for a loan modification. Lenders typically assess the borrower’s financial situation to determine whether the modification will result in a sustainable payment plan. Factors such as income, debt-to-income ratio, and the property’s value are taken into account. Borrowers should also be cautious of scams and work only with their lender or a HUD-approved housing counselor.

Steps to Apply for a Loan Modification

- Contact your lender as soon as you anticipate difficulty making payments.

- Gather all necessary financial documents, including pay stubs, bank statements, and tax returns.

- Write a detailed hardship letter explaining your situation and why you need assistance.

- Submit your application and maintain regular communication with your lender throughout the review process.

- Carefully review the modification agreement before signing to ensure you understand the new terms.

Conclusion

Loan modification can be a lifeline for homeowners facing financial hardship. By working proactively with lenders and exploring available options, borrowers can often avoid foreclosure and regain control of their financial future. While the process may require patience and documentation, the long-term benefits of preserving homeownership and financial stability make it a worthwhile endeavor.

Leave a Reply